As Financial Services Splinters, Banks and Fintech Require Standards More Than Ever

The splintering of financial services is no longer something that might happen or will happen – this has happened, and seems to be fairly well accepted. “There’s an app for that” can be said for almost every major (profitable) sliver of the financial services portfolio of business.

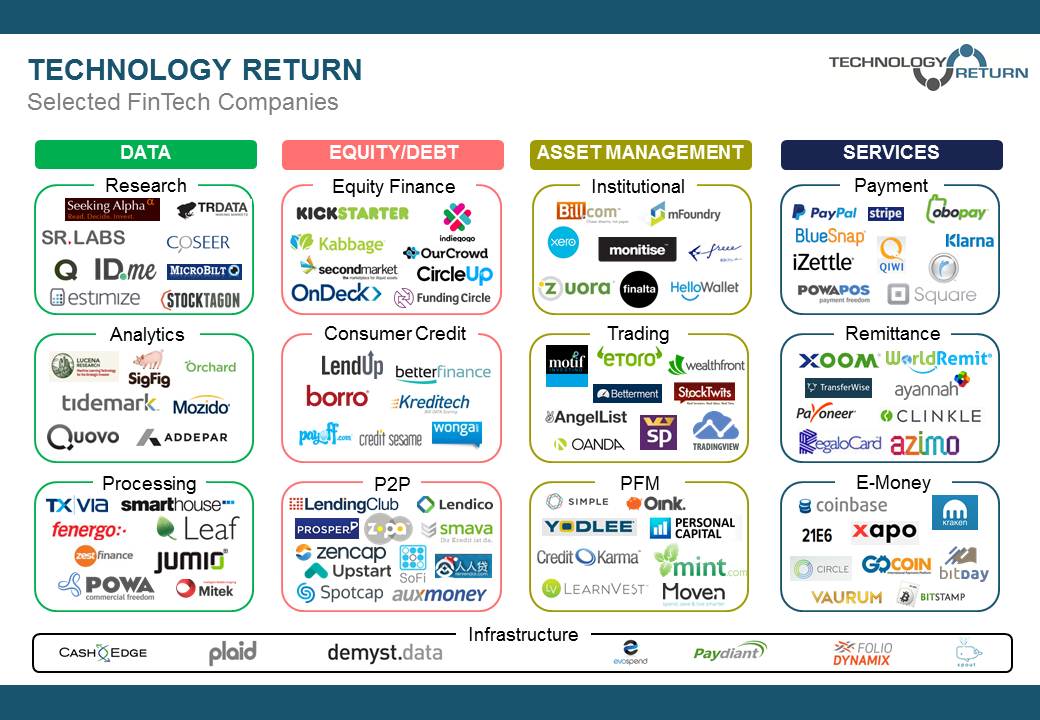

I won’t inundate you with examples, but I do love a good infographic and here are a few that illustrate this reality:

Selected-FinTech-Companies.jpg

My point is that a) this is happening in a big way and b) both banks and financial service providers are coexisting and will need to coexist for the time being and into the foreseeable future.

There has always been a need for standards in financial services – banks spend significant funds on integration. One of the motives behind the BIAN (Banking Industry Architecture Network) {Full disclosure, I am a member and supporter of the BIAN} has been to create open standards that banks and software vendors can align to. This goal if achieved would help to create increased interoperability between banking software and between banks.

Since this group began the challenge has only increased and now there are more players and the line between what is software and what is banking is blurring. We now see challenges between Fintech providers – or between major tech players and fintech.

Yes developing standards sounds very boring – but I’m sure there is a non-boring way to define the fabric that will allow for innovation rather than repetition. How many times will we need to invent the payment header? Let’s agree on the fundamentals and invent the interesting stuff.

The direction of financial services for both traditional banks and fintech players seems to be heading into the direction of API led integration, but we are going to have (even more of) a real mess on our hands in a few years if the payload and semantic layer is not defined and agreed to.

{kind=link}

{kind=link}

{kind=link}