Fintech Players Up the Ante on Comprehensive Credit Reporting

Image credit: Cafe Credit

Image credit: Cafe Credit

In March 2014 the Australian Parliament rubber stamped new Credit reporting & Privacy Laws that enabled Credit Providers (CPs) and Credit Reporting Bureaus (CRBs) to commence voluntary Comprehensive Credit Reporting (CCR).

Australian lenders are well behind on CCR, much to the detriment of Australian borrowers, argue many fintech startups. Compared to the major four banks, fintech CPs suffer from large information asymmetries when it comes to assessing the credit risk of a potential customer. Many new lenders claim that if they were provided with access to repayment histories and a more detailed break down of the lending obligations a customer has outstanding, loan pricing could be more far more discretionary and potentially cheaper for a vast number of Australians.

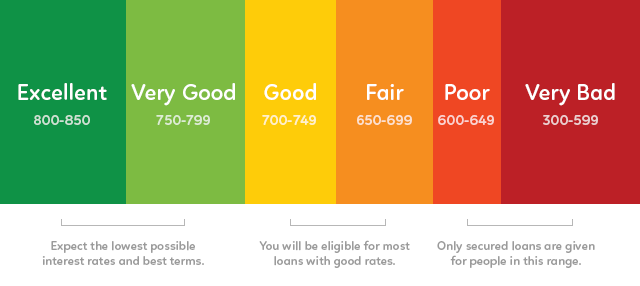

A recent study by Veda tends to support this claim, showing a borrower’s creditworthiness increases when CCR data is available. Using the CCR data it holds on 24 percent of the retail Australian credit accounts it has on file, Veda’s study found the average score for an individual once CCR data was incorporated was materially higher than without.

So if CCR data is generally positive for both sides of the lending/borrowing equation, why is the Australian financial sector dragging its feet? And why is it so hard to work out what lenders are participating in CCR? Surely this is a competitive advantage for a financial institution and a benefit they can offer their account holders? Most likely because this stranglehold on customer data is one competitive moat incumbent financial institutions are relying heavily on going forward.

And it certainly is a deep and powerful moat at that. For no matter how slick and clever the delivery of your lending product is, if CRB data is a key input into whether or not you on-board a customer, then you’ll always be at the mercy of a competitor with better overall data they can use in conjunction with a credit score. Especially a competitor like a bank who holds the vast proportion of data points that make up the proposed CCR framework and is no doubt already leveraging them to their full advantage.

While many lenders are innovative at the front-end, it’s hard to be truly innovative at the back-end (where credit assessment takes place) when data isn’t readily available. A few brave players overseas have tried to disrupt this thinking by doing away with traditional CRB scores altogether. SoFi is one such fintech lender. It’s yet to be seen how this will play out in the long term.

Government intervention

Australia’s 2014 Financial System Inquiry concurs with the broader fintech industry view that the benefits of CCR far outweigh the potential negatives often touted by CCR detractors. Recommendation 20 of its comprehensive report stated the Australian Government should:

Support industry efforts to expand credit data sharing under the new voluntary comprehensive credit reporting regime. If, over time, participation is inadequate, Government should consider legislating mandatory participation.

In 2015, the Government’s response to the inquiry’s recommendation was relatively lacklustre, stating:

The Government agrees to support industry efforts to implement the CCR regime, but will not legislate for mandatory participation at this stage. The CCR regime has been in place for a little over a year and authorised deposit-taking institutions are still in the process of working to participate in the regime.

It has now been a solid two years plus since the new legislation came into effect. Given the opaqueness of CCR implementation across the lending sector, it is unclear how effective the call for voluntary participation has been.

Ratesetter is one fintech lender who has put its money where its data is. In December of last year it claimed it was, “the first Australian lender to fully implement Comprehensive Credit Reporting (CCR) data sharing with Veda, Australia’s leading credit bureau.” Obviously if fintech lenders want the industry to take steps towards CCR, then leading the charge is vital.

Consumers are slowly waking up to the fact that creditworthiness can be a powerful negotiating tool with a lender. A consumer led, bottom up approach may indeed help fan the flames for faster CCR implementation by the industry. Pre-election, the Labor Party campaigned on driving mandatory CCR. If it keeps the heat on for a Royal Commission into the banking sector then this byproduct issue may get some national attention.

Daily Fintech Advisers provides strategic consulting to organizations with business and investment interests in Fintech. Jessica Ellerm is a thought leader specializing in Small Business. ![]()