Consumers Are Still Wary of Digital Wallets (Zelle Isn’t Helping)

The introduction of yet another bank-branded digital wallet service hasn’t exactly shifted the world of payments on its axis.

The introduction of yet another bank-branded digital wallet service hasn’t exactly shifted the world of payments on its axis.

Citi Pay, Citi Bank’s digital wallet (and P2P service, thanks to the bank’s integration with the ever-expanding Zelle network) launched in the U.S. yesterday.

Citi customers can now use the wallet for online and in-app transactions, enabled through the bank’s merge with Mastercard’s Masterpass — which also enables customers to make purchases at Mastercard merchants at the point of sale, using NFC terminals so long as the customer is using an Android device — while the transactions are protected via tokenization technology.

With the rising popularity of services like Venmo, banks are turning to these types of services — bank-branded digital wallet services, such as Citi Pay or Chase QuickPay — to gain consumers.

Those consumers, however, seem to be remaining wary; not only do consumers now have a glut of digital payment options, but the numerous banks signing on to Zelle’s network might actually be making payments more complicated, according to those consumers:

Zelle attaches your mobile # or email to one bank. If you have more than one bank accounts, you are SOL cc @scottbelsky @mdudas #venmokiller

— Vaibhav Puranik (@i_vp) July 5, 2017

That doesn’t mean consumers aren’t using these types of services — Chase QuickPay is only slightly less popular than Venmo, according to some studies — but the continuous march of inter-connected digital wallet rollouts might be causing a fair number of consumers to stick with what they know.

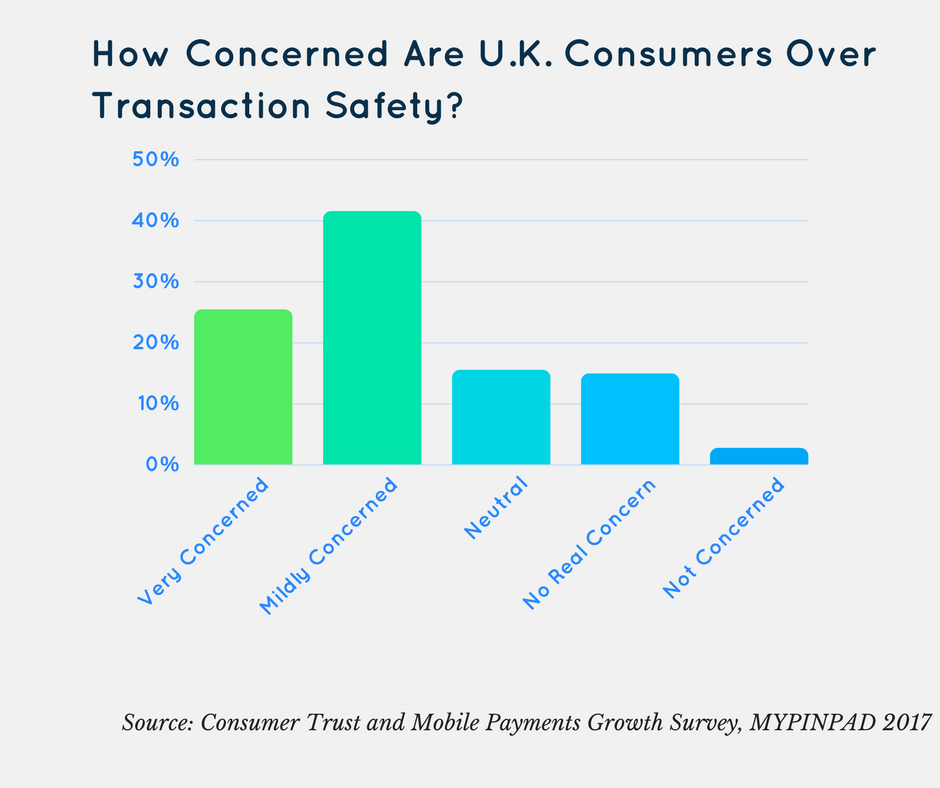

PayPal, for instance, remains one of the most popular payment choices for consumers, while security concerns and bugs continue to stall the adoption of others.