Study Shows Strong Relationship Between Credit Score Review and Credit Score Increase

Can regularly checking your credit score actually help improve your results? We wanted to know the answer to that critical question, so Credit Sesame partnered with Megan Hunter Antill and Jessica Yu, Ph.D., candidates in Quantitative Marketing at Stanford Graduate School of Business, to find out. We conducted an analysis of consumer behavior patterns and credit score trends using data from Credit Sesame’s base of more than 15 million registered members, one of the largest among consumer credit management platforms.

The resulting study demonstrated a relationship between credit score review and credit score improvement. This finding shows that members who are engaging with their credit score details can realize value beyond the identity theft protection and borrowing preparation benefits often emphasized by many financial planning experts and credit monitoring platforms. Additionally, we saw that some consumers might benefit from a gentle nudge toward engaging with their credit-related information.

The Potential for Real Financial Impact

Our examination of a full year of anonymized data from Credit Sesame members showed that consumer monitoring of credit-related data can be a predictor of positive future credit score trends.

Overall, in our analysis of the data, members who returned and checked their scores in the first six months after signing up saw an average improvement of almost 10 points during that period.

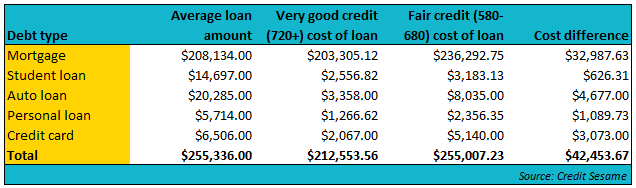

This kind of change in score can have a very real day-to-day financial impact because credit scores are the most significant factor in determining a consumer’s interest rate for a loan, credit card or any line of credit. The 10-point score gain seen by the members who were active in the first six months could translate to significant dollar savings in the cost of their credit.

A 10-point score change may seem minor, but for a consumer on the cusp between two credit score ranges, just one point can tip the scale in either direction. Mortgage lenders, for example, tend to offer interest rates in increments of one-eighth to one-quarter of one percent, with each higher credit score range qualifying for a slightly lower interest rate.

If a consumer whose score increased 10 points qualified for an interest rate of 4.0 percent instead of 4.125 percent on a $250,000, 30-year fixed-rate mortgage, she could save more than $6,500 over the life of the loan. If all other factors are unchanged, this consumer could opt for a smaller loan and lower monthly payment, or apply the savings to discount points, closing costs, or some other expense related to the loan.

Engagement May Be a Predictor of Results

To conduct the study of the data, as a first step, we examined usage patterns and changes in credit scores for members in our database.

As a baseline, first, we analyzed how members’ credit scores change when they sign up for a credit management service — in this case, Credit Sesame. Within just the first 6 months of the data set we saw that more than 61 percent of members had an increase in their credit score.

Furthermore, some members improve even more. We found that of the 61 percent with increased scores:

- 48% improve more than 10 points

- 18% improve more than 50 points

- 4%t improve more than 100 points

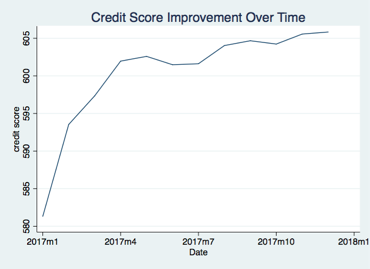

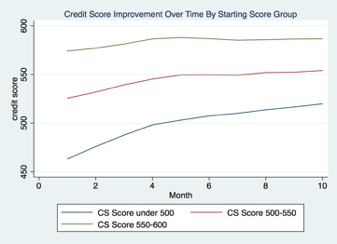

In particular, those members with the most to gain had the most improvement. Those who started with credit scores under 500 improved by more than 70 points on average after one year of membership on the credit monitoring platform. The cohort of members who started with the lowest scores also had the fastest improvement.

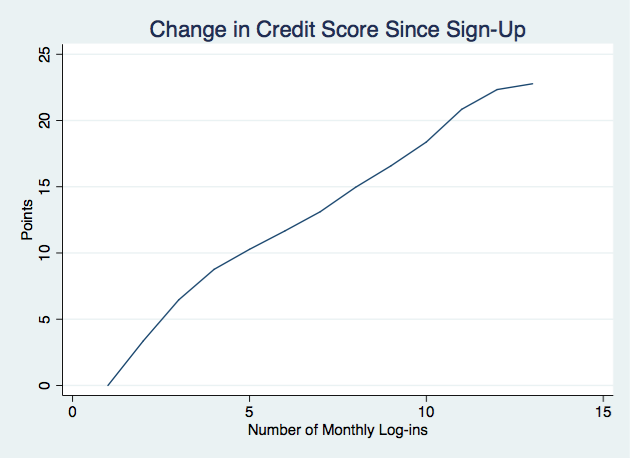

Next, we saw some correlational evidence for how credit scores change with the number of logins. As the number of logins grows for a user, their credit score also increased. It is important to note that this analysis does not control for the amount of time on the platform. The results could also reflect that people who sign up already intend to make changes to improve their score.

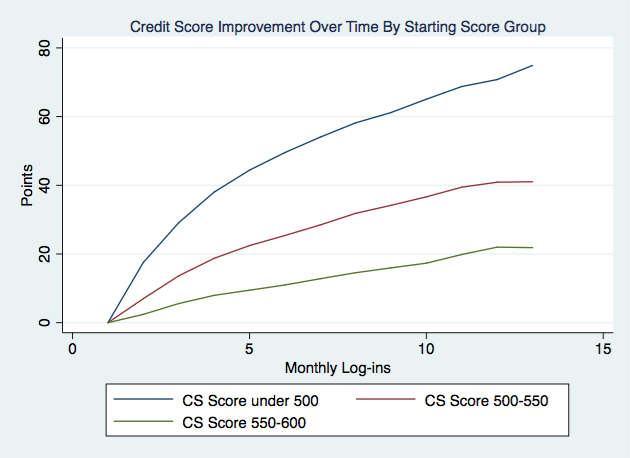

When examining the frequency of members’ score review behavior, we also saw a faster rate of increase in credit scores for members with lower scores. This is similar to the pattern of change based on credit score level that we found in our time-based analysis for the first six months of membership.

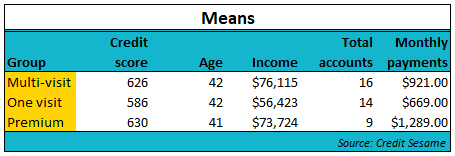

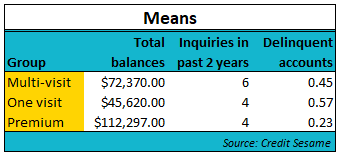

At the same time, we saw that members who only visit the platform once and do not return have, as a group, much lower incomes, monthly payments and total balances. These members also tend to have more delinquent accounts and lower credit scores than members who continue to return to Credit Sesame.