SympliFi launches remittance alternative to enhance access to credit in Africa

U.K.-based startup SympliFi is launching a loan product for customers in developing countries in Africa backed by collateral from family members in the U.K.

With SympliFi’s model, which launched in late August, U.K. residents with family in Zimbabwe can offer collateral with local Zimbabwean financial institutions, allowing the family back home to take out a loan and build credit. The company is branding this offering as an alternative to remittance incumbents like Western Union and MoneyGram, as well as startups like Remitly and TransferWise.

“Because (families) can’t access financial services locally, their only alternative is to call their family member in the U.K. and say, ‘Look, can you just send me money and I’ll pay you back’,” said Maurice Iwunze, co-founder of SympliFi. “We’re trying to deliver the underlying financial services for which those funds typically are used.”

SympliFi is targeting families that need money for a range of use cases, including school supplies, covering funeral costs, small businesses and healthcare. To this end, the company is partnering with a network of financial institutions in the sub-Saharan countries of Zimbabwe, Tanzania and Nigeria that specialize in these areas.

Loan terms are between two and three months; amounts range between £200 and £500 ($244 to $609). Banking and other partner institutions set the interest rates, which Iwunze would not disclose.

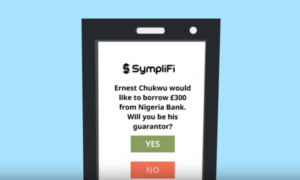

SympliFi’s first partner is Educate, a Zimbabwean lender that specializes in loans for school fees and supplies. To access funds, borrowers advise Educate of the individual in the U.K. who can offer collateral, which usually is between 50% and 100% of the total loan size. Educate then will use SympliFi’s platform to send a text or email to the guarantor in the U.K., who puts up collateral through a debit card. Customers and guarantors need to provide their names, addresses and a picture of their passport or driver’s license to confirm their identities.

Once the loan is paid back, the guarantor receives a refund of the collateral deposit in full. If the borrower in Zimbabwe defaults, the remainder of the collateral deposit is deducted before the money is refunded. A borrower defaulting doesn’t hurt the guarantor’s credit score, but it could hurt the borrower’s score.

According to the Brookings Institute, only 18% of people in sub-Saharan Africa have access to credit. Iwunze said the Educate partnership will appeal to families that can’t afford to buy all of their school supplies upfront. Over time, if borrowers make timely payments through SympliFi, they can get better interest rates and need less collateral to cover their loans. Iwunze said the goal is to eliminate the need for guarantors once borrowers upgrade their credit scores.

SympliFi doesn’t charge any fees to the guarantor, but the company charges a fee to the local partner institution. Iwunze wouldn’t offer details on how much partner institutions pay.

SympliFi is planning to expand to Tanzania and Nigeria within the next five weeks. Iwunze said the company will partner with lenders that focus on small businesses and microlending. It’s open to guarantors in the U.K. for now, but SympliFi is looking to expand into the European Union and, eventually, the U.S. The company hopes to launch health insurance and funeral care loans, and it would like to find new ways to underwrite guarantors other than just collateral.

In displacing remittances, however, SympliFi faces well-established competitors and the challenge to change customer habits. A recent Aite Group study estimated that remittances were a $689 billion industry in 2018, with Africa and the Middle East accounting for almost $111 billion. The company’s remittance startup competition has received major funding this year, with Remitly, TransferWise and WorldRemit bringing in nine-figure funding rounds in recent months.

Talie Baker, a senior analyst with Aite’s retail banking and payments practice, said SympliFi has created a difficult business model because people who receive remittances might not have the means to pay back a loan and people who leave their home to find work in the U.K. might not have collateral. “(SympliFi) may need to target a segment other than the typical immigrant leaving home due to lack of employment opportunities,” she noted in an email.