Upgrade bridges the gap between credit cards, installment loans

Banks and digital lenders may be throwing their weight behind point-of-sale loans instead of credit cards, but personal loan company Upgrade is launching a product that straddles both product categories.

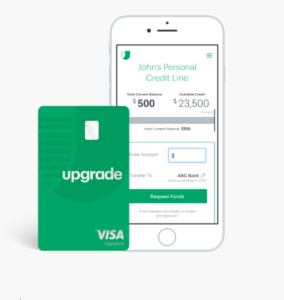

The Upgrade card, launched Thursday, functions like a credit card at checkout, but purchases are turned into payment plans that can last one, two, three or five years. Customer eligibility for the card is based on data beyond traditional credit bureau information, including customers’ cash flow and expenses. Instead of revolving credit, Upgrade turns customers’ monthly balances into installment loans.

“If you only make the minimum payment on a credit card, it’s going to take you 25 years to pay it off,” said Renaud Laplanche, co-founder and CEO of Upgrade and the co-founder of Lending Club. “Credit cards don’t encourage that responsible behavior of paying down your balance every month. The personal loan does.”

The Upgrade card offers credit limits of between $500 and $50,000 depending on assessed risk. According to Laplanche, terms are more financially healthy for customers than traditional credit cards. The installment loans start at 6.49% APR, but the rates can go as high as 29.99%. The loans can help build customers’ credit scores if they pay them off in time, according to the company. Like credit cards, however, Upgrade charges late fees, which Laplanche said vary by state.

With the Upgrade card, the company hopes to improve its underwriting and provide better loan terms with a clearer line of sight into customers’ spending data. The loans are provided by Cross River Bank, while Sutton Bank is the card issuer.

See also: Lending Startup Upgrade Opens Personal Credit Line, Shares Plan for Mobile App

Upgrade launched more than two years ago, and the company has originated more than $2 billion in personal loans. In addition to revenue from interest and late fees, Upgrade makes money from its marketplace, which sells consolidated loans back to banks.

Leslie Parrish, senior analyst at Aite Group, said the Upgrade card won’t be as helpful to consumers who typically pay off their credit card balances each month. “While converting a balance to an installment loan would be more expensive for those borrowers who might otherwise pay off their card each month, it should result in cost savings for those tempted to otherwise make only the minimum monthly payment,” she explained.

Bank Innovation Build, on Nov. 6-7 in Atlanta, helps attendees understand how to “do” innovation better. It is designed to offer best practices, to guide the innovation professional to better results. Register here.