Data Can Build Engaged Bank Customers, If You Pick the Right Set

How should FIs leverage data to better engage customers?

Well, according to Cardlytics President and co-founder Lynne Laube, you follow the money.

“Three households who look identical demographically…are going to get the exact same credit offer,” said Laube at the DataDisrupt conference today. “They look very different when you understand where and how they are spending money, versus their demographics.”

Cardlytics, which collects data on 20% of all the U.S. card purchases (or about one in every five card swipes), uses data analytics to break down consumer purchase data–where they shop, and what they buy– rather than just consumer demographic data.

So how exactly does that help banks?

Cardlytics leverages consumer purchase data to benefit both the customer, and the banking institution; the customer gets personalized financial product and credit offers from Cardlytics, while banks, in turn, form a more engaging relationship with their customers.

The company sits its software behind a bank’s firewall, where consumer data is both protected and tracked. A BofA customer, for instance, is known to Cardlytics only by an ID number issued by the bank, but that customer’s purchases are cataloged.

The company sits its software behind a bank’s firewall, where consumer data is both protected and tracked. A BofA customer, for instance, is known to Cardlytics only by an ID number issued by the bank, but that customer’s purchases are cataloged.

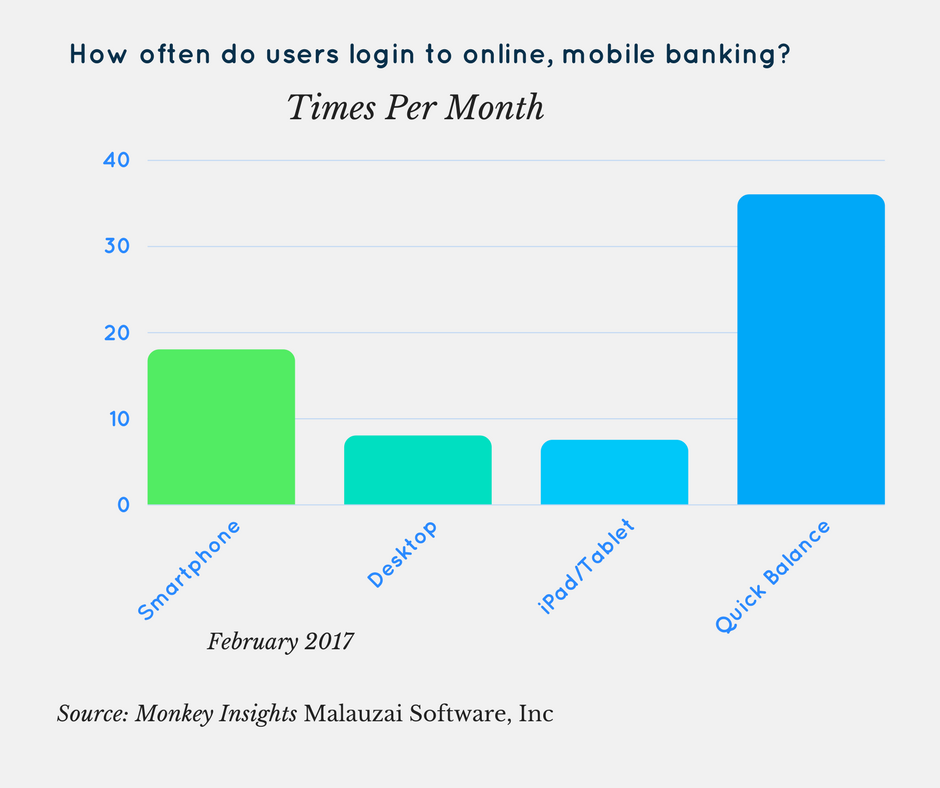

“We’ve essentially connected the use of purchase intelligence to anywhere a customer goes digital,” said Laube. She noted that the average consumer in the Cardlytics network uses online banking 12 times a month, and mobile banking 22 times per month.

According to Laube, Cardlytics works with 1,637 financial institutions, which have seen an average of 27% decrease in attrition, combined with a 7% increase in card spend.

The alternative approach to collecting consumer data here raises the importance of what kinds of data financial institutions should focus on, because picking the wrong set means a lack of actionable insight, and thus, a lack of engaged customers.