Data shows smaller FIs are far behind because of weaker mobile technology

Smaller banks and credit unions are under increasing pressure from larger banks and tech-centric financial services companies.

New data shows why significant gaps in mobile banking capabilities are complicating these FIs’ struggles to keep up. Underlying macro trends where big banks continue gaining share, data on product and feature-level propositions provides a granular view of the difficulties smaller banks and credit unions face.

Features as customer engagement drivers

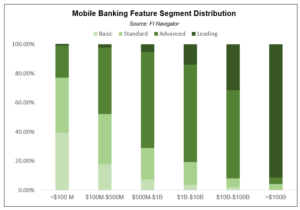

An analysis of the level of sophistication of FI mobile offerings, for example, reveals that there are drastic differences across the asset spectrum. Virtually all FIs with more than $100B in assets have leading mobile feature sets compared to only 30% or fewer of FIs below the $100B asset mark.

Leading features include rewards management, PFM modules, credit score data, debit card on/off, among others. While not all banks would consider these to be table stakes, having a compelling mobile offering helps with both customer engagement and customer satisfaction, areas where data also shows smaller players lag larger FIs.

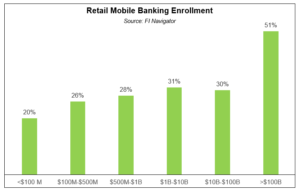

Retail mobile banking enrollment

Compared to larger banks, which currently have retail mobile enrollment rates above 50%, smaller financial institutions are only able to enroll 20% to 30% of their customer base.  This could be somewhat unproblematic now, but rapidly shifting customer expectations and evolving distribution models will push banks with low mobile engagement to the sidelines, gradually eroding their service and branch-led propositions.

This could be somewhat unproblematic now, but rapidly shifting customer expectations and evolving distribution models will push banks with low mobile engagement to the sidelines, gradually eroding their service and branch-led propositions.

Customer satisfaction indicators

When smaller financial institutions manage to engage their customers through digital channels, satisfaction rates are also lower compared to larger banks. Banks with more than $100 billion in assets consistently outperform smaller competitors in mobile app satisfaction, by as much as ratings of 4.4 to 3.4. For customers that have their primary relationships with banks that offer subpar experiences, in many cases the switching costs are currently too high. As the performance gap widens, however, unsatisfied customers will be drawn to banks that offer full functionality at the level they expect and be compelled to switch.

Profitability implications

What do banks with limited mobile features stand to lose? Analyzing data by level of mobile feature sophistication shows that, beyond engagement and customer satisfaction, mobile banking feature segments also correlate with financial performance. FIs with leading mobile features enjoyed ROEs almost 300 basis points above those with basic functionality and 100 to 200 basis points above those with standard or advanced capabilities.

While these results don’t necessarily imply a causal relationship between mobile offering sophistication and profitability, financial institutions with subpar offerings clearly have a steep mountain to climb. Their survival, at least in part, hinges on their ability to do so.

At INV Fintech, a startup accelerator and banking consultancy, we believe the right approach includes a combination of a deeper data-driven exploration to benchmark current capabilities and a product roadmap that can be catalyzed through strategic fintech partnerships.

Rodrigo Suarez is the principal of INV Fintech. To learn more about FI Navigator data used in this piece, click here. To learn more about INV Fintech, click here.