Study Shows Strong Relationship Between Credit Score Review and Credit Score Increase [Page 2]

Information Avoidance

While the gains among consumers who achieved rising scores were interesting, we looked a bit deeper at members with declining scores to understand a phenomenon known as information avoidance.

Our usage data showed a pattern. Members whose scores were on a downward trend seemed to actively avoid information about their credit score status. Individuals with decreasing scores were less likely to log in again in the future after signing up for an account on the credit monitoring platform.

Researchers have studied and defined this condition as “a behavior that is intended to prevent or delay the acquisition of available but potentially unwanted information.”[1] Prior studies have documented that in many settings individuals sometimes choose to avoid information even when it is free and useful. For example, millions of people sign up for health and fitness tracking services to record caloric intake and weight through apps, wearable devices or even a scale. Although individuals who register for these services clearly place a value on obtaining this information, some subsequently never or rarely check the data after signing up.

Our study echoed the results of this other research that shows that information avoidance tends to happen more when individuals believe they are performing badly or worse than before. Those who sense they are underperforming are less likely to seek out information in the future.

The Benefit of a Gentle Nudge

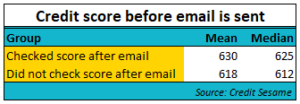

To further understand and confirm the information avoidance effect, we also examined user actions following reminders about the platform. We saw that following an email to a randomized set of members, those with the highest rate of check-ins were those with higher scores. This pattern reinforced the finding that those who are performing poorly are less likely to check their information.

We were encouraged that receipt of an email from the platform caused a higher rate of check-ins by members, given the positive correlation between active monitoring and credit score gains. In the two weeks, before the email was sent, 8 percent of members in this sample logged in and viewed their score. After the email, 25 percent of members in this group logged in.

Interestingly, we saw this effect in the data even if the content of the email was not primarily intended a reminder. An email on unrelated topics also seemed to serve as a reminder about the availability of information on the platform and the opportunity to check.

We also looked at members who were on a declining credit score trend before the email was sent. We found that if these members logged-in after the email, their score improved by 0.5 points in the next month. This may seem like a small gain, but as noted above, a single point could translate to thousands of dollars in savings.

Conclusion

We sought to find the relationship between user engagement with credit score data and the impact on financial health as measured by future credit score. Our findings show strong evidence that regularly checking scores is correlated with credit health.

Our industry can continue to play a role in helping consumers live healthier financial lives by providing incentives and reminders to take actions that could improve their credit and financial health. The interest among consumers to maintain their credit health is there, as evidenced by sign-ups for services such as ours and others. As financial technology organizations, our mission must be to use our ever-evolving set of data science tools in ways that continue to encourage consumers to act.

Megan Hunter Antill and Jessica Yu are Ph.D. candidates in Quantitative Marketing at Stanford Graduate School of Business. Pejman Makhfi (@pmakhfi) is the CTO of Credit Sesame, a leading personal credit management platform with over 15 million members to date. A Silicon Valley tech veteran and expert published on outlets such as VentureBeat and the California Management Review, Pejman has over two decades of experience in personal finance, fintech, AI and machine learning projects.

[1] Sweeney, Kate et al., Information Avoidance: Who, What, When and Why, Review of General Psychology, December 2010