With Softbank investment, working-capital marketplace C2FO closes $200m round ‘for global expansion’

The business-to-business credit market just got a big boost from Softbank’s Vision Fund.

C2FO, a nine-year old working capital digital marketplace, on Wednesday raised $200 million in a Series G funding round led by Softbank Vision Fund, with participation from Temasek and Union Square Ventures. The company declined to disclose the round’s valuation.

The Leawood, Kan.-based company will be using the funds primarily for “global expansion,” Colin Sharp C2FO’s senior vice president told Bank Innovation. He declined to elaborate on specifics, but noted that part of establishing a global presence is making sure that C2FO has “the right technology across the world.”

C2FO claims to use proprietary algorithms to create a “seamless match” between accounts receivable and accounts payable to dynamically price the value for early payment in real-time. The company has raised a total of $397.7 million of funding to date.

“There’s a difference in how you engage with suppliers, say in China, than the U.S.,” Sharp said. It’s both the “technological needs of each market,” and supplier support functions “in local language and local timezone.” In addition to focusing on global expansion, the company also plans “to innovate and bring new products to market,” Sharp said. He declined to elaborate.

Working capital is essential for companies to innovate, build products and hire employees. C2FO estimates that the liquidity flows its platform allows can fund between 10 million and 20 million new jobs. A company spokeswoman pointed to the car industry’s shift to electric as an example.

“Every single part of the supply chain needs to invest in innovation and needs liquidity to do this,” the spokeswoman said. “Innovation won’t happen without it.”

Softbank’s Vision Fund’s backing is a bet on the scalability of the C2FO platform and a vote of confidence in its growth prospects. The fund is currently supporting such large financial startups as digital lender and challenger bank OakNorth, business lender Kabbage and Indian mobile payment startup Paytm.

C2FO already has a global network, working with more than 300,000 businesses across 173 companies. It’s also a partner of Citibank.

The spokeswoman said that current banking regulations make it “very difficult and unattractive for banks to lend to smaller businesses,” specifically “those with weaker credit ratings, [which are] often those that need liquidity the most.” C2FO fills “that void,” Sharp said.

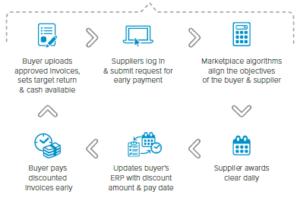

The company connects buyers and suppliers via an online platform. If the supplier doesn’t have enough liquidity to produce the buyer’s order, the supplier can request an early invoice payment, offering the buyer a discounted rate. It saves both companies money in the long run, according to C2FO, since it lets the suppliers offer a discount that would cost them less than the interest they might pay if they took out a loan. According to the company’s website, it allows companies to turn “receivables into cash flow and payables into income.”

The field of dynamic discounting overall is “becoming an asset class on its own,” said Aite Group senior analyst Enrico Camerinelli. Camerinelli added that in the business-to-business marketplace, the investment and the company’s consequential global spread — to which he estimates the company will put the bulk of the investment — means that SME companies “may count on additional sources of liquidity, while buyers can better utilize their free cash availability.” Funds might also be used to develop applications and algorithms to incorporate in the marketplace and to onboard more small-business buyers, he noted.

Despite the large investment, Camerinelli expressed reservations about the model over the long term.

“The model of the account receivables and payables matching marketplace is valid, but not sustainable in the long run if only offered to large multinationals, as they do today,” he explained. “They must incorporate also smaller companies on the payables — in other words buyers’ — side.”

A potential downside to the platform, he noted, would be that it’s not integrated with other working capital platforms, such as Primerevenue, Demica or Taulia, “forcing the use of multiple systems to coordinate and manage,” Camerinelli said.